There is a quote that states, “If you think education is expensive, try ignorance”. Unfortunately, this quote is true on SO MANY levels. While many people associate the word ignorant with being dumb or stupid, it’s simply the condition of being uneducated, uniformed, or unaware. After graduating from Spelman College, I made both smart and dumb decisions regarding my student loan debt. I was told by my aunt that paying your student loans is a great way to establish credit. I put in an extra effort in paying Sallie Mae, so much that I had it paid more than year in advance. This was smart, ignorant, and sometimes dumb at the same time. It’s smart because I really never had to worry about forgetting to pay the bill. I felt extremely proud of myself for not being another “irresponsible” 20 something. It also revealed my ignorance because I should have been using that extra payment every month to pay down the balance NOT pay it in advance. I ended up paying interest when I could have been slaying the balance, which ultimately shortens the life of the loan. However, it wasn’t until I was in between jobs and not paying on the loan at all because the next due date was a year from then that I started digging a hole that I am still trying to get out of four years later. For one, my interest was accruing at about $8 a day, so a lot of the money I thought I was saving was now been tacked back on to the overall balance. It got worse when after the year was up, I still wasn’t working and I accepted an offer to postpone my payments for a year. That was back in 2011 and after yesterday’s phone call to Sallie Mae, my decision to postpone is still hurting my finances.

I pay about $200 a month for my student loans and recently got a series of letters saying that if I qualify I should sign up for automatic billing, which would let Sallie Mae automatically deduct money directly from a specified account every billing cycle. The incentive you ask? A .25% reduction in my student loan interest…equaling about $50 a month and $600 per year. I called Sallie Mae on yesterday, only to find out that I did NOT qualify. Apparently, if you post pone your loan at ANYTIME over the life of the loan, you lose eligibility for any interest rate reduction. Had I known this I would have been the never postponed my loan, but this secret penalty was never in any of the documents I agreed to. Looking back I would have rather roughed it out. So I guess the quote rings true. My education was expensive but my then financial ignorance could cost me more in the end.

We would LOVE to hear your thoughts?

FACEBOOK, TWITTER, PINTEREST, RSS Feed ,

Email SMC: shemakescents@gmail.com

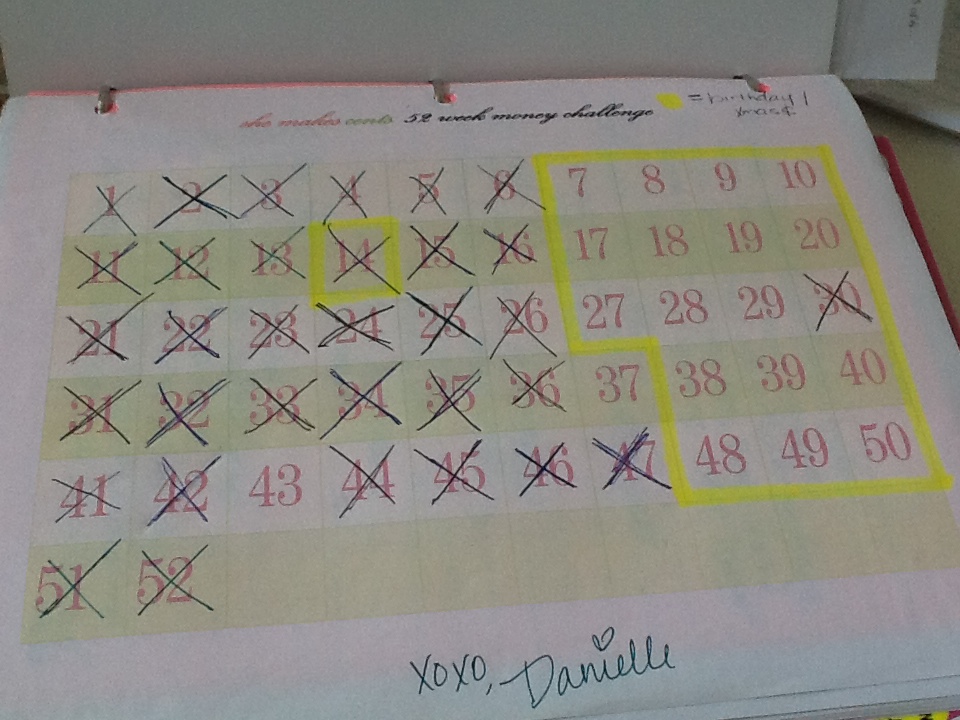

January 16, 2014

January 16, 2014